This quick breakdown explains how car insurance costs work in Tennessee and what factors affect your monthly rate.

Quick Answer:

Minimum car insurance in Tennessee requires $25,000 per person, $50,000 per accident for bodily injury, and $25,000 for property damage. While this meets legal requirements, it may not fully protect you in a serious accident.

Most drivers in Tennessee carry the minimum required car insurance to stay legal—but what many don’t realize is that minimum coverage may not be enough to fully protect them in a serious accident.

Tennessee requires liability coverage of $25,000 per person, $50,000 per accident, and $25,000 for property damage. These limits meet state requirements, but they are designed to satisfy the law—not necessarily to cover real-world costs.

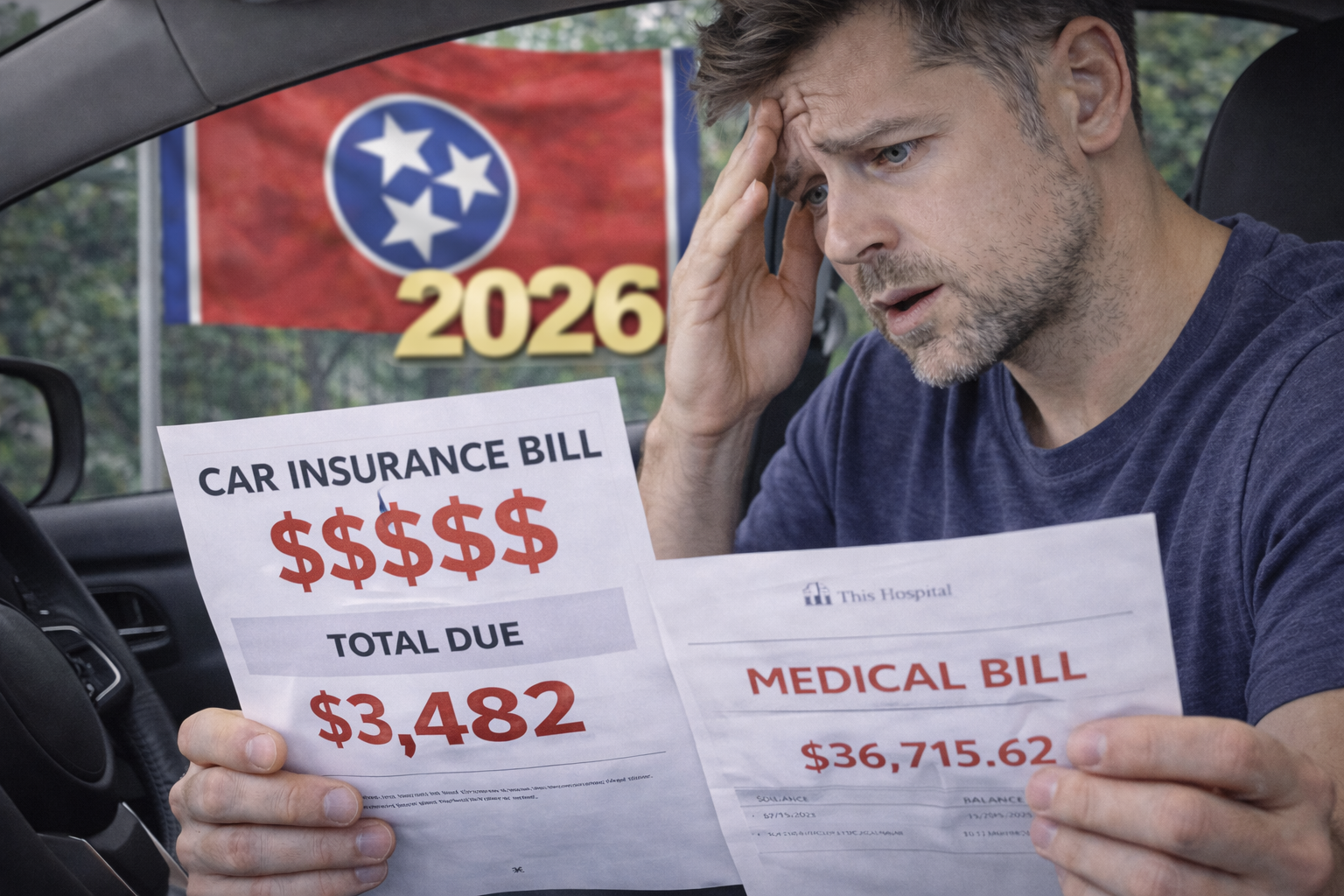

In many cases, even a moderate accident can exceed these limits quickly, leaving drivers responsible for the remaining balance out of pocket.

Minimum liability coverage only pays for damage or injuries you cause to others. It does not cover your own vehicle or your own medical expenses. That means if you’re involved in an accident, your financial exposure could be higher than expected.

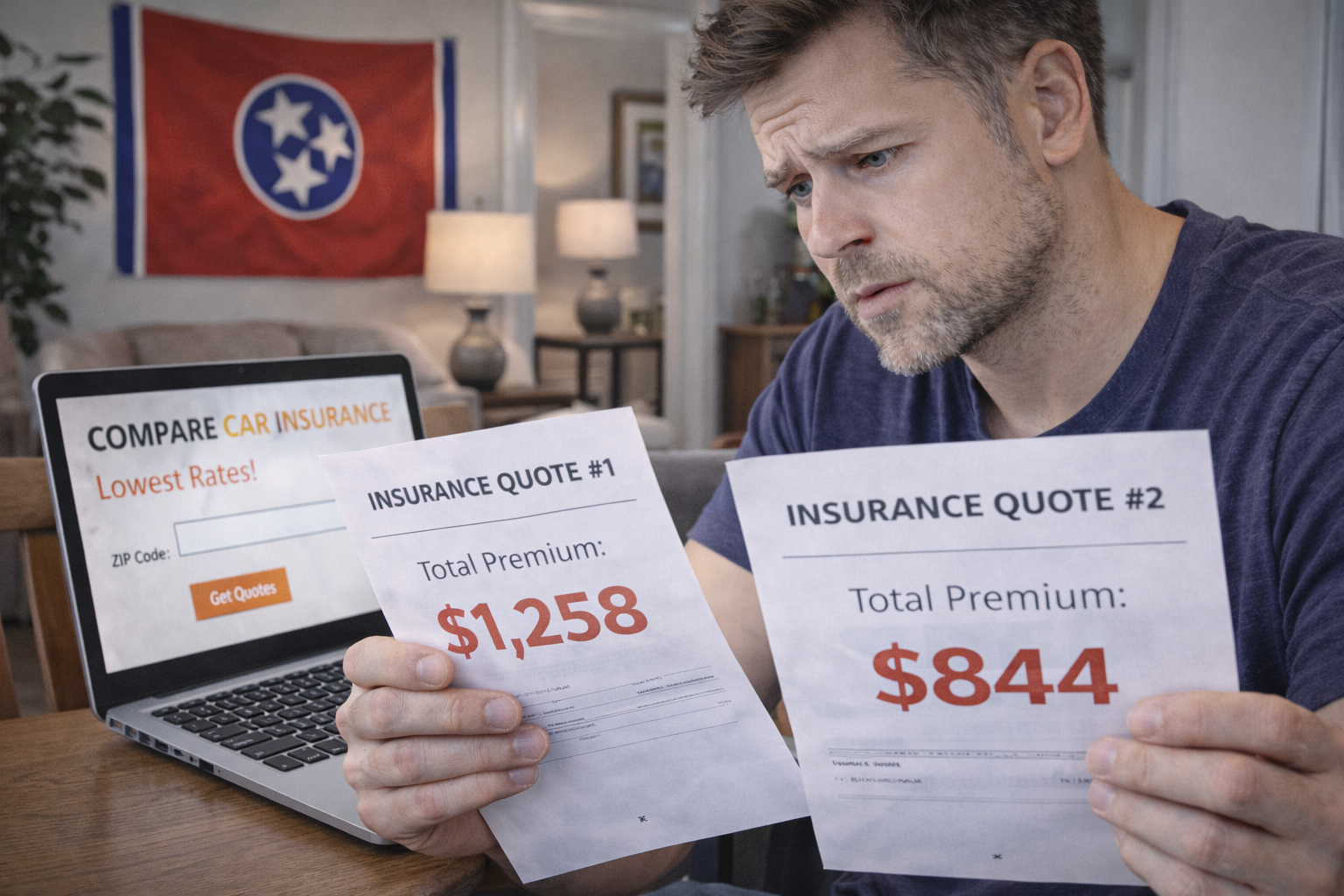

Because of this, many drivers in Tennessee choose to carry higher coverage limits or additional protection depending on their situation.

👉 Get a Free Car Insurance Quote Review and See If Your Coverage Is Enough

What Most Tennessee Drivers Don’t Realize

Minimum coverage is often misunderstood. Many drivers assume it fully protects them, but it’s really just the baseline required to legally drive.

The reality is that accidents don’t follow minimum limits. Costs can exceed coverage quickly, especially when multiple vehicles or injuries are involved. When that happens, the remaining balance doesn’t disappear—it becomes your responsibility.

In situations like this, some drivers also look into having access to legal guidance when unexpected issues come up—especially when dealing with liability, claims, or disputes after an accident.

👉 Learn how affordable legal protection for drivers works and what it can help with

That’s why reviewing your coverage periodically can help you avoid unexpected financial risk and make sure your policy actually fits your needs.